The Weekly Update

Week of July 24, 2017

By Christopher T. Much, CFP®, AIF®

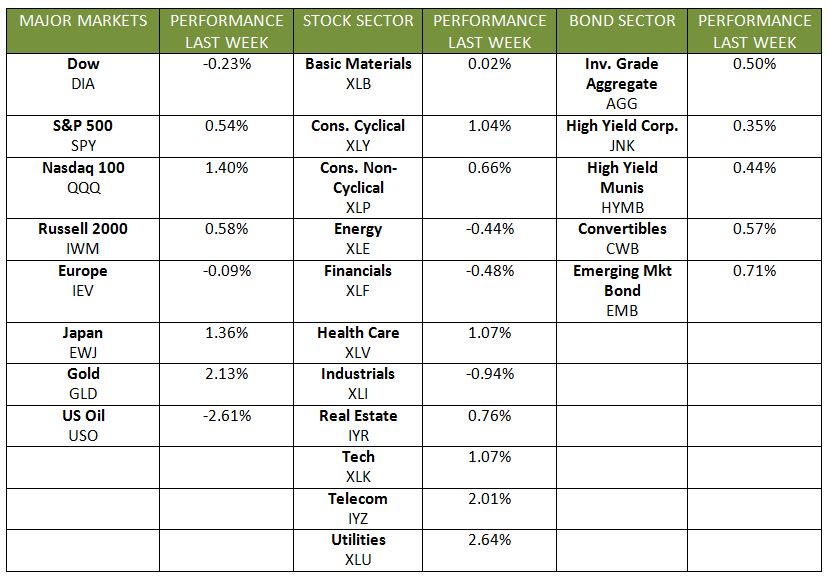

Last week, the Dow, S&P 500, and NASDAQ again hit record highs. The midweek peaks fell by Friday, though market performance remained strong. By week’s end, the Dow dropped 0.27%, and the S&P 500 and NASDAQ dipped on Friday but closed up 0.54% and 1.19%, respectively. The MSCI EAFE finished with a 0.46% increase.

Corporate Earnings Drive Growth

Analysts noted that stocks were particularly “strong” last week due to generally robust Q2 corporate earnings reports. With roughly 20% of S&P 500 companies reporting, corporate earnings should remain solid through the quarter. So far, 73% of reporting companies beat their estimated earnings per share, and 77% have higher-than-expected sales against a 5-year average.

Weakened Dollar Continues

The dollar continued its downward trend, dropping 1.3% during the week. So far, our currency has fallen 8.1% since the start of 2017. A weakening dollar will boost companies with exports or overseas business. As such, the U.S. consumer will take a hit, since a falling dollar causes price increases on imported goods. The latest fall started last week after the Fed expressed concerns over low inflation.

By and large, European markets reacted negatively to the falling U.S. dollar, and uneven EU corporate earnings reports did not help either. With the euro’s value against the dollar rising to its highest point since January 2015, the value of EU company exports and overseas earnings measured in dollars will fall.

Other Key Market Developments

Here are some other key developments in fundamentals from last week:

- Housing Tensions Relax: Housing starts jumped to a 1.215 million annual rate, the first gain in three months. Similarly, housing permits increased to a 1.254 million rate, the strongest numbers since March. Homebuilders are cautious, however, with the Housing Market Index and Components falling 3 points in July. The rising cost in lumber—due to tariffs on Canadian softwood—has builders concerned, as homebuyers will ultimately pay higher prices.

- Jobless Claims Fall: July’s employment numbers look hopeful as the initial jobless claims for the week of July 15 dropped to 233,000, far below the consensus estimate of 246,000. The numbers should help lower July’s overall unemployment rate and suggest that—despite low wages and productivity—labor demand remains high.

- Oil Prices Drop: Oil prices fell over 2% on July 21, after reaching a 6-week high earlier in the week. The drop followed news that OPEC increased July production by 145,000 barrels daily while U.S. stockpiles largely decreased, contributing to the temporary price hikes.

A Busy Week Ahead

This week will be busy. More housing news starts the week, and expect Wednesday’s Fed meeting to get some attention, though interest rates should not increase. Further, Friday’s Gross Domestic Product (GDP) Price Index and Consumer Sentiment Index will be of interest to markets.

Though the news from Washington can dominate the headlines, remaining focused on key drivers of market performance is key. Contact us if you have questions as to how the past week’s markets may influence your portfolio. We are always happy to help.

ECONOMIC CALENDAR

Monday: Existing Home Sales

Tuesday: FHFA House Price Index, Consumer Confidence Index

Wednesday: New Home Sales

Thursday: Durable Goods Orders, International Trade In Goods, Jobless Claims, Chicago Fed National Activity Index

Friday: GDP, Employment Cost Index, Consumer Sentiment